Blackk Mortgage Brokers Gold Coast

Mon-Fri 9am to 5pm

After-hours appointments available

11/76 Township Dr, Burleigh Heads QLD 4220

99.6% of home loans approved in 2025

No Obligations

5.0 Stars Based on 151 user reviews

I'm Victor, founder of Blackk Mortgage Brokers. Since 2007, we have been the home loan specialists helping Gold Coast families and first home buyers make smarter financial decisions when buying, building, renovating and investing in property.

Before we apply for your home loan, we get you home loan ready. That means reviewing your full picture first, then advising you with a clear action plan on how to increase your borrowing capacity so you can safely maximise what you can borrow.

Then when you're ready to buy, the banks will quickly approve your home loan putting you in the best position to successfully buy.

With access to over 50 banks and lenders, we can secure you the best interest rates and have the expertise to structure your loan around where you’re headed, not just where you are today. The whole time you are supported by our award winning customer support team who check in regularly and guide you through every stage of the process.

Buying your first home is exciting but it is a lot to get your head around. We've guided hundreds of Gold Coast first home buyers through pre-approvals and QLD's lending rules. That includes the first home buyers grant QLD, the first home guarantee scheme, and our QLD stamp duty guide, making the process smooth and stress-free.

Clear guidance, no service fee

660+

first home buyers helped in the past year

8

QLD first-home buyer incentives

Buying your first home is exciting but it is a lot to get your head around. We've guided hundreds of Gold Coast first home buyers through pre-approvals and QLD's lending rules. That includes the first home buyers grant QLD, the first home guarantee scheme, and our QLD stamp duty guide, making the process smooth and stress-free.

Clear guidance, no service fee

660+

first home buyers helped in the past year

8

QLD first-home buyer incentives

QLD 2024 Bankwest Broker Of The Year Awards

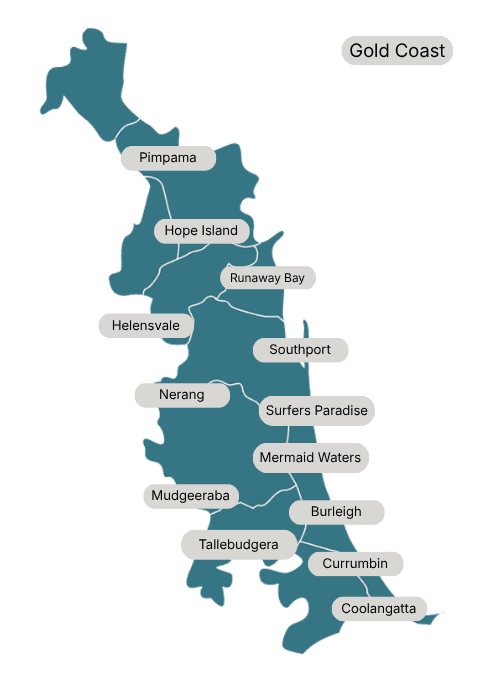

Location is everything. Where you buy on the Gold Coast directly affects your home loan approval, your insurance costs and your long-term capital growth. Here are four often overlooked factors to consider before making an offer on a property.

Canal homes spread across the whole of the Gold Coast like those in Palm Beach, Burleigh Waters, Broadbeach Waters, Isle of Capri and Paradise Point as well as low lying areas around waterways are popular but may come with lending complexity and potential extra insurance costs. Checking flood maps and insurance quotes early helps identify risks before committing.

Lenders treat buildings with active management rights or high short-stay concentration as higher risk, often putting a limit on what you can borrow. Properties with receptionists in the building fall in this group. Check with us before you commit so you know your options.

Buying in a sought-after school catchment zone can significantly increase resale value on the Gold Coast, as primary and high school choices often influence where families decide to live. Properties within popular public school zones tend to attract stronger demand from buyers planning for long-term family living.

When buying a unit in a high-density area, be aware of floor spaces under 50 square metres. It may impact what you can borrow and resale value. Surfers Paradise and Broadbeach have a concentration of this stock. We know what the building's lenders will and won’t touch.

50+

lenders compared to get the right loan for your needs

19+

years serving the Gold Coast with expert advice

2200+

families secured their homes with Blackk Mortgage Brokers

50+

lenders compared to get the right loan for your needs

19+

years serving the Gold Coast with expert advice

2200+

families secured their homes with Blackk Mortgage Brokers

Some of the most expensive errors aren't caused by the market. They come from assumptions and oversights during the buying process. Our team can help advise you on what to watch for.

Online listings have improved. They've also become more selective about what they show. Aim to attend around 20 open homes in your target area before making offers. Burleigh, Palm Beach, Robina, wherever you're focused. You develop a real sense of value quickly when you're walking through properties in person rather than scrolling through photos. When you're ready to move, our guide on how to make an offer on a house covers the next step.

On the Gold Coast, garages and carports are sometimes converted into extra rooms without council approval. A home may be marketed as having four bedrooms when council records say three. The lender's valuation will reflect council records, not the listing. That discrepancy can affect your borrowing capacity, which means you are overpaying and create problems later in the process. Your conveyancer will check records before you commit.

Real estate agents represent the seller. Most are professional and helpful. None of them are on your side. Get an independent building and pest report from your own inspector, or we can refer you to someone from our network. It's a small cost against what a missed structural problem can turn into.

No Obligations

We compare 50+ lenders, pre-check policy fit, and structure your loan around your goals, so you can buy with confidence, not guesswork.

That includes guidance on borrowing limits, valuations, and the steps that strengthen approval the first time.

You’re limited to one lender’s rules and process.

You’ll usually get a single or limited set of options, generic guidance, and slower back-and-forth, especially if your situation isn’t straightforward.

There’s less flexibility to shape the loan structure around your future plans, and more risk of surprises at the valuation or approval stage.

Refinancing, buying before you sell, or self-employed? See refinance your home loan, bridging loans, or self-employed home loans for those specific situations.

5.0 Stars

Based on 151 user reviews

Rob & Laura

“Victor and the team went above and beyond to ensure we secured the property we wanted. They took the time to explain the steps involved during the buying process, their communication was excellent and knowledge of the market second to none. These guys were a pleasure to deal with and we would absolutely use again. Highly recommend.”

Dylan & Bree

“My fiancé and I are both self-employed and we were concerned about finding a lender who would cater to our situation. Thankfully, Victor and Christal made the entire financing process a breeze. They were extremely prompt with all communication, super professional, offered an enormous amount of industry knowledge, and most importantly, they helped us secure our family home...

Isabelle & Wayne

“Thank you Victor and the team you made our home loan journey a happy, stress free experience. We were updated at every step and Victor’s advice in the early stages was invaluable to us securing our loan. We need more community minded, person centred business’ like this. Would recommend Blackk Mortgage Brokers to anyone looking for genuine financial advice with no hidden agenda.”

Two types of calls, depending on where you’re at. If you need loan approval within the next four weeks, we go straight into your numbers and personal situation so we can map the quickest, safest path to approval.

If you’re three to twelve months away, we cover how much you can borrow, how much you need to save and the exact steps to get your application ready. Most people find the confusion clears up immediately. After the call, we send through a personalised action plan and follow up along the way.

Borrowing capacity depends on lender credit policy, not just income and savings.

Key factors include:

On the Gold Coast, things like floor space in high-density buildings, flood overlay classifications and holiday letting arrangements can also affect how lenders assess a loan. We calculate borrowing capacity using current lender policies so the figures hold up when it counts.

A pre-approval is an early assessment of your financial position. It helps you understand your price range and negotiate with more confidence, but it still requires nearly a full application and isn’t a final decision.

Formal approval happens after you’ve signed a contract. The lender assesses your full application, reviews the contract of sale and completes a valuation on the specific property.

We focus heavily on preparation before either stage so the formal approval is as smooth as possible.

Timeframes vary depending on the lender, the complexity of your situation and their current queue. A straightforward application can come back in one to two days. More complex ones like self-employed income and unusual property types can take ten days or more.

Once we submit, we manage all communication with the lender, respond to credit questions and follow up on valuations. Careful preparation before submission is what reduces delays.

Lenders need documents to verify identity, income, assets, liabilities and credit history.

**

PAYG**

Self-employed

We tell you exactly what’s required based on the lender we’re using so you’re not asked for unnecessary paperwork.

In most cases, nothing. Lenders pay us after settlement, similar to how banks pay their own lending staff. You don’t pay the bank’s lending manager when you walk in, and you don’t pay us.

If a fee ever applies due to a specific or complex situation, we explain it clearly before any work proceeds.

Yes. Comparing lenders is only part of what we do.

**

We help with:**

We also factor in how different lenders assess properties commonly found on the Gold Coast, including waterfront homes, high-density apartments and properties with holiday letting arrangements.

Yes. We regularly help Gold Coast clients review existing home loans to see whether refinancing or restructuring will save money or open the next step toward a property goal.

This may include comparing rates, negotiating with your current lender, assessing switching costs and reviewing how the loan is set up. The aim is to make sure your loan still suits your circumstances.

FIFO income is generally accepted by most lenders, but how it’s assessed varies. The key factors are whether your contract is ongoing or fixed-term, whether the income includes allowances and overtime, and how long you’ve been in the role. Short-term contracts or income heavily reliant on allowances can be discounted or excluded entirely by some lenders.

Lender selection matters here. Some are more experienced with FIFO applicants and will assess the full income picture more fairly. We work through your contract structure and income breakdown before choosing a lender, so the figures hold up rather than getting reduced at assessment.

Yes, and the Gold Coast has more of them than most markets. Flood overlays and insurance costs on canal properties, proximity to high-voltage power lines, serviced and holiday-letting apartment buildings, high-density units under 50 square metres, FIFO and non-resident income situations, and renovations without council approval can all influence lending decisions.

We identify these early so they don’t become problems at the valuation or approval stage.

We're based in Burleigh Heads and work with clients across the Gold Coast from Coolangatta and Palm Beach in the south, through Robina, Varsity Lakes and Surfers Paradise, to Southport, Hope Island and the northern corridor. In-person, phone or video, whatever works for you.

"Most buyers on the Gold Coast are ready to buy long before their broker tells them they are."

— Victor, Founder, Blackk Mortgage Brokers

Mon-Fri 9am to 5pm

After-hours appointments available

11/76 Township Dr, Burleigh Heads QLD 4220