How To Reduce Your Home Loan Repayments

Written by Written by Victor Kalinowski, Mortgage Broker and Founder of Blackk

Written by Written by Victor Kalinowski, Mortgage Broker and Founder of Blackk

If you have a mortgage (or two) right now, you may be feeling concerned about how long you are able to continue making loan repayments for and how to cover household bills.

After a spate of interest rate changes, those with variable-rate mortgages may be feeling the pinch.

The increased cost of borrowing has not only affected mortgage repayments but has also impacted overall household budgets, making it challenging for many to manage their finances effectively. It’s crucial to review your financial situation regularly and consider options like refinancing or seeking professional advice if you’re struggling to meet repayments.

In this post I want to give you some clear guidance on the steps to take to first get clarity on where you stand financially, and then tell you how to reduce your home loan payments (both owner occupier and investment loans).

1. First, get clarity on your income and expenses for the next 6 months.

2. Switch to making only the minimum mortgage repayment required.

3. Can you redraw advanced repayments from your home loan?

4. Do you need to consolidate multiple debts into your home loan?

5. Should you refinance your home loan?

Please get in touch if you want to talk about your situation in more detail and you can book a call with me here.

Right now I recommend everyone have a look at their income and expenses.

You need to get clarity on your situation for at least the next 6 months, so you can see exactly where you stand.

While it is tempting to put your head in the sand and ignore what is going on, never has there been a more important time to get a handle on this.

Knowing your bottom line will help you to determine what action you may need to take.

Take stock of the following:

What is your expected monthly income for the next 6 months or so:

Salary / wages expected

Government benefits expected?

How much cash do you have access to right now?

Is there any way to earn extra income?

How many weeks/ months can you get by for?

What are your necessary expenses and debt repayments?

What are fixed or ones you can not get out of?

What expenses can you cancel or put on hold?

Once you have this clarity:

Do you need to put mortgage/s on hold for 6 months?

Whilst I always recommend paying off your home or investment loan sooner with extra repayments, times of financial pressure cab be an exception to this.

If cash flow is tight, call your bank or go online and reduce your loan repayments to the minimum required for now.

When your home cash flow is back to a level you are comfortable with, then I recommend you go back to making extra repayments.

Many people have been diligently making extra repayments above the minimum required in the past.

If you have done this, you should be ahead on your home loan repayments.

Depending on the type of home loan you have, you should be able to access some or all of this money:

On a 100% variable rate home loan – you can access all extra repayments made;

On a split loan (both fixed and variable rates) – you will only be able to redraw money on the variable portion of your home loan;

Loan is on a 100% fixed interest rate – you won’t be able to redraw any funds however under special circumstances you may be able to so call your bank directly.

If you have a variable loan (or a portion of your home loan is on a variable interest rate), then you should be able to access this money through your redraw facility for no extra charge.

You can use this money to make your minimum loan repayments and for general living expenses / bills.

To check how much you are ahead in your repayments, have a look at your online banking. This will show as ‘available funds’ or ‘redraw’ on your home loan account.

You can usually transfer this money straight into your linked transaction account or linked offset account and you’ll get access to the money fairly quickly.

Some lenders will have a daily maximum limit you can transfer, so just be aware of that.

Remember also that you will need to advise the bank that you want to make the minimum (or at least lower) home loan repayment for what ever period of time you choose. If you don’t alter them, the direct debit will remain the same.

For most people, their debt repayments are by far the biggest expense of their salary/s, so let’s take a look at how we can save you some money there.

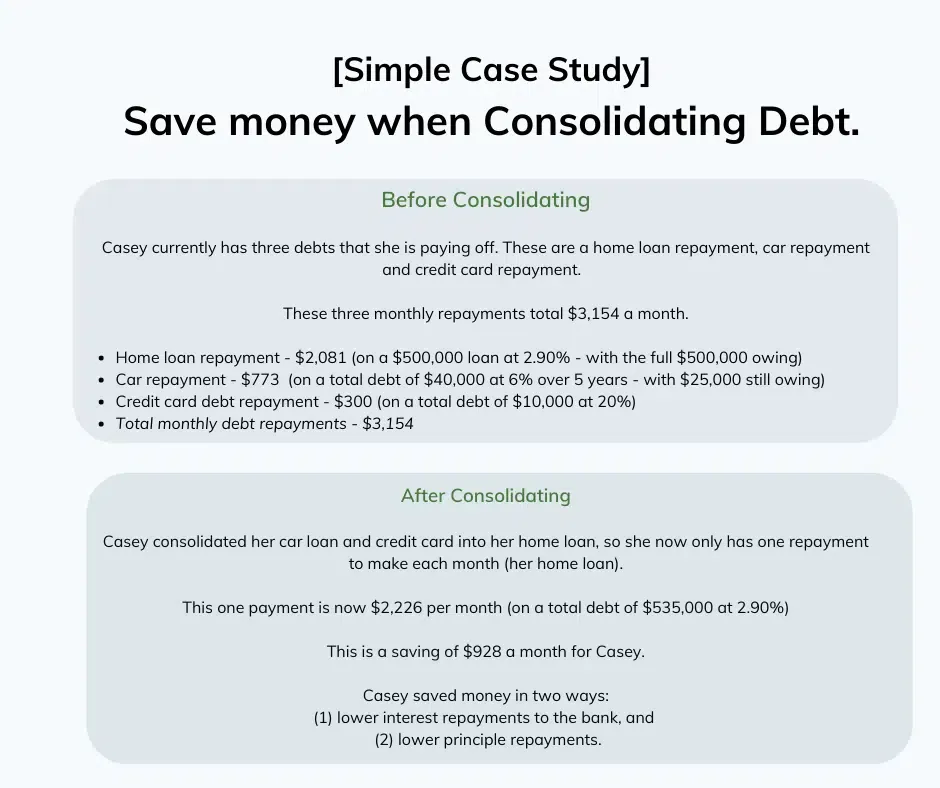

If you are currently making multiple repayments across credit cards, a car loan and your home loan, then lets have a look at what would happen if we consolidated this into your home loan.

When we consolidate your debt, this can either be done with your existing home loan lender or we may need to refinance you to another lender if we can find you a better deal elsewhere.

If you do have multiple debts and loans you are repaying please give me a call to go through this.

As you can see, there are substantial savings to be made, however we really need to run these numbers for your individual situation.

Refinancing your home loan or investment loan could be beneficial for some of you, especially if you have not refinanced in the last 2 years or more.

This probably means the bank doesn’t have you on the sharpest rate and given interest rates have fallen in this time, now is a very good time to review this.

It is best to give me a call or book one here if you would like to do this.

If you need help with how to reduce your home loan repayments, please get in touch with us. We have expert knowledge in home loan payment reduction and low-interest-rate mortgages.

Victor Kalinowski

Mortgage Broker and Founder of Blackk

I’m Victor Kalinowski and a Brisbane Mortgage Broker at Blackk Mortgage Brokers. I’ve helped thousands of people get loans for their homes and investment properties.

99.9% Approval Rate

Insider advice to negotiate making a successful offer on a home

Award Winning Mortgage Broker

If you are happy with the service from your current lender, but would like a better deal.

Work with Victor, not with random brokers

If you are happy with the service from your current lender, but would like a better deal.

with 99.6% first time success rate

No Obligations

Subscribe to get tips on home loans and property straight to your inbox

By downloading you agree to receiving occasional and only useful emails from us.