Why A Debt Consolidation Mortgage Saves You Money

Written by Written by Victor Kalinowski, Mortgage Broker and Founder of Blackk

Written by Written by Victor Kalinowski, Mortgage Broker and Founder of Blackk

Home loan consolidation involves combining multiple debts, such as credit cards and personal loans, into a single mortgage. This approach usually provides a lower interest rate. This makes repayments easier and may lower your monthly payments. Saving you money and time when it comes to managing your repayments.

The strategy is relevant if you have:

An owner occupied home loan; AND

At least one other debt such as credit / store cards, car loan, personal loan, buy now pay later; AND

You want to stay with your current bank, OR if refinancing you want to borrow less than 80% of the value of your home.

Key benefit:

This can save you money and improve your cashflow each month by lowering your total monthly debt repayment.

Based on the assumption that we roll some or all debts into your home loan as it will have the lowest interest rate.

If you are looking for the most effective way to reduce your monthly expenses so you can save more, then rolling all or some your debt payments into your home loan might be the right strategy for you.

Many of us are now starting to feel the pressure of rising costs of living and rising interest rates.

So far in 2022, the RBA has already increased rates several times, including June’s leap of 0.5% and all banks have passed on some, or all these rises to their customers.

As I am sure you are aware, the predictions are that there are more rate rises to come over the next 6 to 12 months.

I see a lot of family budgets and I can tell you that it is quite common that the biggest fixed expenses each month are debt repayments.

Home loans, car loans and a maxed out credit card often can be the biggest chunk of fixed expenses.

As interest rates rise again, you may find yourself starting to feel concerned about how you will be able to afford all your monthly loan repayments

You can also watch me explain this on you tube if you prefer.

You will also be interested in this post on 3 best ways to reduce your mortgage repayments including a strategy on switching to lower variable rate and a strategy for property investors.

Let’s get into it!

What we’re finding is that some people who are in this situation are feeling the pressure on their cashflow already.

They are going, hey look …

I’ve got my home loan over here that I’m paying and that’s been manageable.

But now I also have a few other loans and debts that I need to repay, and I’m finding it’s all getting a bit tight with the rate rises we’ve had so far.

I don’t really know how I am going to handle even more rate rises – I don’t think I have enough cash each month to make each repayment.

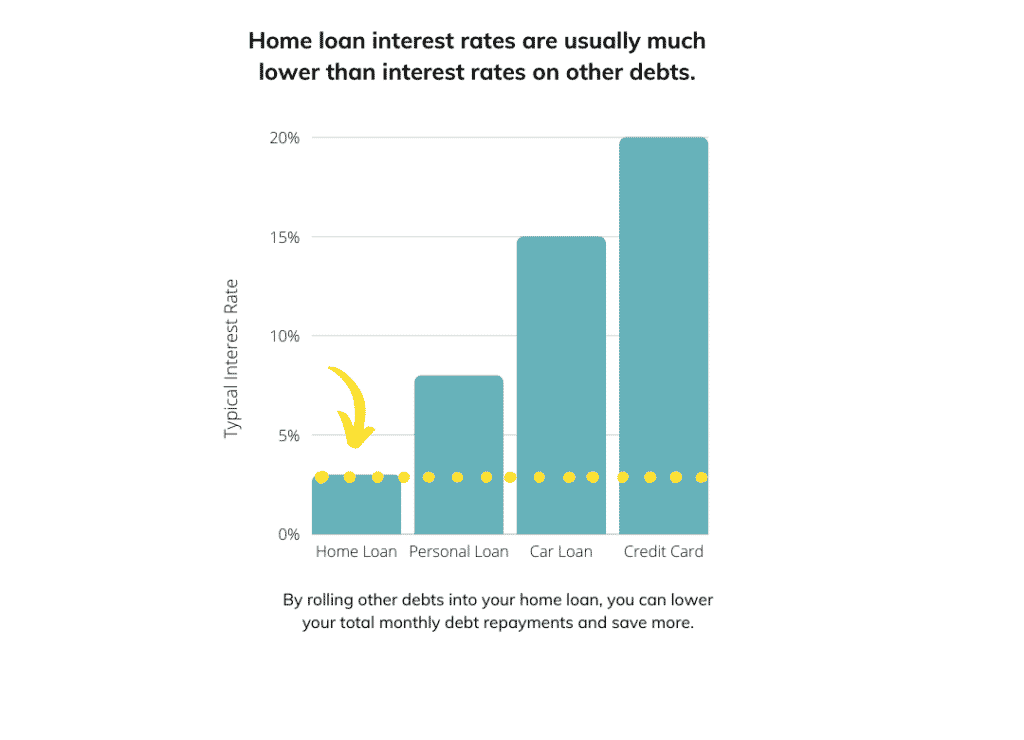

The reason why this strategy saves you money is that you are likely paying a much higher rate of interest on your car or motorbike loan, personal loan, credit cards and buy now pay later loans – than you are on your home loan.

Home loans are typically between 2% or 3% depending upon a few different scenarios.

Whereas a lot of these credit cards have interest rates over 20% and personal loans are somewhere between 5% and 12%.

By consolidating these loans into one it can reduce the amount of interest that you pay to the banks overall and it also frees up your cash flow.

We had some clients in May, who reduced their weekly loan repayments by a massive $280 by using this strategy.

They were making four different debt repayments each month across a motorbike loan, car loan, credit card debt plus their home loan.

Not only were the interest rates considerably higher on these other debts, it can also be stressful managing cashflow around multiple debt repayments dates.

However, by rolling those loans into the home loan they reduced their payments by about $280 less per week.

The way this works, is we apply for an increase in your home loan – equal to the total value of your other debts.

You then draw down on these funds and pay off your other debts like your car loan and credit card.

Then you can close those loan accounts down, and you’re left with:

One loan (your home loan), which means one simple repayment each month; and

A lower repayment overall

Your home loan repayment should now be less than what all your other debts combined were before the debt consolidation.

In this example, this person saved $1,668 a month by rolling their car loan and credit card debit into their home loan.

Before consolidating debt, the monthly repayments across all three debts was $3,860.

We increased the value of the home loan by $54,100 (car loan + credit card debt) and drew these funds down to pay out and close those debts.

We are then left with one monthly debt repayment (not 3) of $2,192 (which is a saving of $1,668 a month).

| Debt | Interest rate | Monthly 'interest only' repayment | Total loan value |

| Home loan | 2.8% | $2,147 | $920,000 |

| Car loan | 15% | $565 | $45,200 |

| Credit card | 20% | $148 | $8,900 |

| Total debts | $3,860 | $974,100 | |

| Home loan + other debts | 2.7 | $2,192 | $974,100 |

| Monthly saving | $1,668 |

We encourage our clients to save as much of the difference that they can so in the event that interest rates rise further that you’ve got that money there set aside to help when you really need it.

Its always better to take control and create a buffer for yourself rather than trying to back track once you are in arrears.

It will be a lot less stressful in the future!

Lenders mortgage insurance

As I’ve mentioned, you need to increase your home loan, to cover the total amount of your other debts.

Debt consolidation is a good strategy right now because of the strong property market.

A lot of people will have substantial equity in their property, more than what they had a year ago.

This means they can increase their home loan, without triggering what is called Lenders Mortgage Insurance.

Lenders Mortgage insurance is triggered when you have borrowed more than 80% of the value of your property and it can be a substantial additional cost for you.

You can get a lower interest rate

It’s also worth knowing that you can often get a much better deal on your home loan at the same time.

This is another little bonus as overall it brings your costs on everything down just that little bit extra.

What this does is it reduces the total amount of payments that you’ve got and also reduces the amount you are paying.

Want to understand more about what’s involved in refinancing? See our complete guide to refinancing here.

My name is Victor Kalinowski and I’m a mortgage broker at Blackk Mortgage Brokers, with offices based in West End (Brisbane) and Burleigh Heads (Gold Coast). If you’re interested in getting in touch for some advice, book a call instantly at a suitable time or call us on 07 3122 3628 today.

If you need help with debt consolidation in Brisbane, Blackk Finance is a top mortgage and refinance broker. We have expert knowledge in home loan consolidation and low-interest-rate mortgages. Explore our services to begin your journey towards financial security with smart property investment.

Victor Kalinowski

Mortgage Broker and Founder of Blackk

I’m Victor Kalinowski and a Brisbane Mortgage Broker at Blackk Mortgage Brokers. I’ve helped thousands of people get loans for their homes and investment properties.

99.9% Approval Rate

Insider advice to negotiate making a successful offer on a home

Award Winning Mortgage Broker

If you are happy with the service from your current lender, but would like a better deal.

Work with Victor, not with random brokers

If you are happy with the service from your current lender, but would like a better deal.

with 99.6% first time success rate

No Obligations

Subscribe to get tips on home loans and property straight to your inbox

By downloading you agree to receiving occasional and only useful emails from us.