Lenders Mortgage Insurance | Avoid or reduce your premium

Written by Written by Victor Kalinowski, First home, Home Building, Investment Property, Next home, Renovating

Written by Written by Victor Kalinowski, First home, Home Building, Investment Property, Next home, Renovating

As a Mortgage Broker, I help my clients reduce or avoid the amount of Lenders Mortgage Insurance (LMI) they pay.

Most of the time I can save them several thousands of dollars, but the better option is to avoid paying it altogether.

This post explains the best ways reduce and avoid paying Lenders Mortgage Insurance, including the latest on the Federal Governments Home Guarantee Scheme.

If you do not have a 20% deposit saved when you go get a home loan, you will need to pay an extra fee called Lenders Mortgage Insurance (LMI).

Read more here on the basic’s of Lenders Mortgage Insurance.

The trigger to pay LMI is:

You have less than a 20% deposit saved to buy a home, based on the value of the property

If you are lucky enough to have a bigger deposit, of 20% or higher saved, then you will not need to pay LMI.

It covers you (and the bank) for the life of your home loan which is typically 30 years.

In saying that though, it’s important to know upfront that if you buy a home today but are planning on renovating your home in 3 years time, you may also pay LMI again when you do a loan increase for the renovations. If you borrow more money, and your equity/deposit becomes less than 20% of the purchase price of the property.

LMI is paid when you home loan settles, which is usually when you take ownership of the property/property settlement.

In terms of how you pay, you can either:

Add it to your home loan which is known as capitalising your LMI, or

Pay for it using part of your house deposit.

I recommend you capitalise the cost of the LMI to your home loan rather than if they pay it out of your deposit, however I can go through this with you.

Yes, LMI needs to be paid when you are borrowing more than 80% of the value of the property (i.e you have less than a 20% deposit).

This includes when you’re buying an investment property, vacant land or building a home.

Just like car or health insurance premiums are different between providers, the amount of Lenders Mortgage Insurance you need to pay will vary depending on 3 things;

The amount of your home loan;

Which lender you are taking out the loan with;

The loan to valuation ratio of the loan that you’re borrowing.

I cover this in more detail below.

These are the five ways to avoid paying LMI:

#1: Have a 20% deposit:

If you don’t have at least a 20% deposit, and you don’t meet one of the other three criteria below, then you will pay LMI.

For example, you would need at least $100,000 as a deposit if the home you’re buying is worth $500,000.

It’s important to remember that if you’re building your first home, you can include the Queensland Government Building Grant as a part of your deposit (at the moment this is $20 000).

#2: Take advantage of the Federal Governments Home Guarantee Schemes:

First home buyers and who fit certain criteria can buy a property and avoid paying LMI

There is some criteria around this, for example:

The value of your property must be under set thresholds

Your income needs to be under set thresholds

Read the full eligibility criteria here

#3: Work in certain professions:

If you work in certain professions accepted by the lenders, then you only need to pay a 15% deposit to avoid LMI.

These are: lawyers, solicitors, accountants, doctor, pharmacist, anesthetists, dentist, physiotherapists, surgeons to name a few.

Keep in mind that you may need to meet other criteria to get this deal and there will often be conditions to the loan as well.

#4: Having help with a family guarantee:

This is where a family member has sufficient equity in their home or investment property and they want to help you out with buying your home.

The family member then commits to provide the required equity as a security guarantee.

For example, if you have 10% as a deposit yourself, then your family can provide the remaining 10% to make up the required 20% to avoid paying LMI.

#5: Get a loan ‘special promotion’

From time to time some lenders will run promotions to target a certain type of loan. The most common promotion is to reduce the threshold to 15% rather than the 20% (i.e. if borrowing $500,000 you need a $75,000 deposit instead).

There are often other requirements to take this promotion, such as you need to pay principle and interest repayments (rather than interest only), they charge a higher interest rate on these loans and they restrict the type of property and the postcode that you’re buying in.

There are 5 ways to avoid paying Lenders Mortgage Insurance when you do not have a 20% deposit saved.

For many people, it’s really challenging to save the full 20% deposit to avoid paying LMI – especially when you’re buying your first home.

For example, let’s say you’re buying your first home and it’s a 3 bedroom Queenslander in Greenslopes at a price of $620,000.

A 20% deposit on this property would be $125,000, plus buying costs like stamp duty, solicitor’s fee’s etc.

This can be very difficult for most people to save upfront.

The good news is, there are still ways you can save money by reducing your LMI premium.

The three big ways I reduce LMI are:

When I run different deposit / loan amounts I find the sweet spot, which is where if a client reduces their loan by a small amount (a few thousand dollars), their LMI premium also drops by more than a few thousand dollars. I cover this one in more detail below.

All lenders charge different premiums so you could save several thousand dollars difference.

If you have loans for both your home and your investment property, don’t have them both with the same lender.

‘LMI Sweet Spots’ came about after analysing lots and lots of different LMI quotes and scenarios for clients to work out how to save them money on their LMI premium.

What I discovered was that in certain circumstances, if you increase your deposit by a small amount (and hence decrease how much you borrow), it can make a really big difference in the cost of LMI.

I’m not talking about increasing your deposit by $20,000 – most people wouldn’t be able to save or find that amount of money quickly!

Instead, I’m talking about increasing your deposit by few thousands of dollars to save double that!

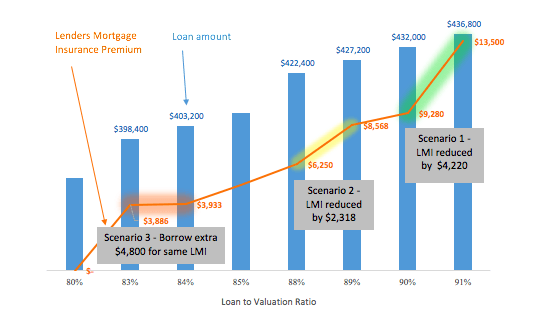

The best way to show you this is through the chart below. If you aren’t a graph or numbers person, don’t be put off. I’ll take you through a simple example.

The loan amount is the blue bar.

The lender’s mortgage insurance payable at that loan amount is shown by the orange line.

You can see that I have highlighted three sections in orange, yellow and green.

These are some examples of ‘sweet spots’ where you can save on your lender’s mortgage insurance.

The best sweet spots happen at LVR’s of 88%, 90% and 92%.

Let’s look at a scenario where we recommend an LVR of 90%.

A client comes to me wanting to buy a home for $480,000.

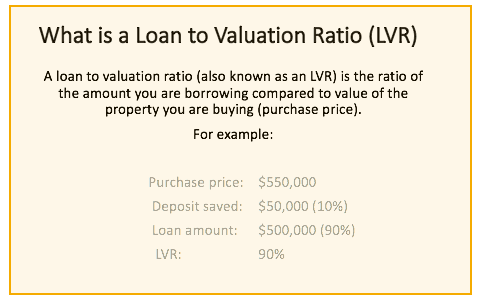

They have a deposit saved of $43,200, so they need to borrow $436,800 with an LVR of 91% (read about LVR’s in the callout box above).

At this deposit and loan amount, the LMI they need to pay is $13,500.

| Purchase price (loan + deposit): | $480,000 |

| Loan amount: | $436,800 (LVR of 91%) |

| Deposit: | $43,200 (9%) |

| LMI premium payable: | $13,500 |

| Total loan amount (Loan + LMI) | $450,300 |

| Repayments on loan (weekly)* | $526 |

Recommendation:

After running these scenarios with a client to investigate we can show what the repayments and LMI cost would be if they have a slightly larger deposit ($4800 in this case). Now that they understand how it works and how their repayments would be lower they can see if it’s worth waiting a little bit longer for their savings to increase.

Lenders Mortgage Insurance

| Purchase price (loan + deposit): | $480,000 |

| Loan amount: | $432,200 (LVR 90%) |

| Deposit: | $48,000 |

| LMI premium payable: | $9,280 |

| Total loan amount (Loan + LMI) | $441,480 |

| Repayments on loan (weekly)* | $515 |

This means their deposit needs to be $48,000 (not $43,200).

This reduced their LMI premium to $9,280 (saving them $4,220).

By putting in the extra $4,800 in deposit, this client ended up borrowing $8,820 less overall (extra deposit of $4,800 + LMI saving of $4,220).

*** Borrowing less means their repayments are also $11 less per week. So let’s say you took out the second option but paid the $526 in repayments – this means you will pay your loan off 1 year and 4 months sooner than you would have otherwise.***

Wrap up: It’s worth considering different LVR’s (deposit to loan ration) to see how tweaking a few numbers here and there can actually save you several thousand in LMI. You will also reduce how much you borrow and lower your loan repayments overall.

Scenario’s 2 and 3 coming shortly in bonus material!

*Based on principle and interest repayments at an interest rate of 4.5% over 30 years.

Simply by changing lenders, you can save hundreds.

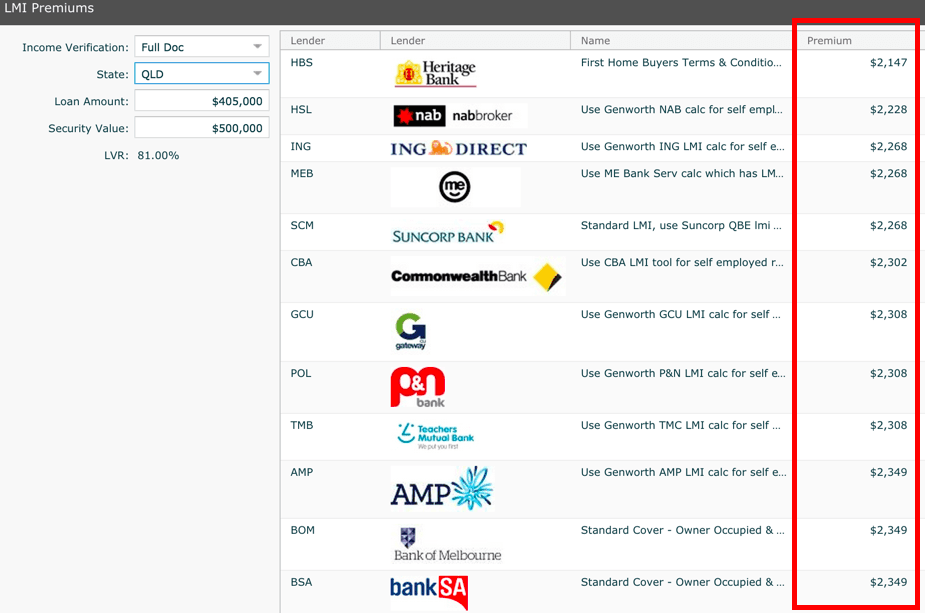

Looking at the table below, this client wanted to buy a home worth $500,000.

They had a $95,000 deposit, so wanted to borrow $405,000 (LVR 81%).

If this client took their loan out with Commonwealth Bank, the LMI premium would be $2,302.

The cheapest LMI premium is with Heritage Bank at $2,147 and the highest is $2,349 which is offered by several lenders including AMP and Bank of SA.

How Does LMI Protect The Lender?

If you stop making your loan repayments, the lender will take ‘possession’ of your property (this term is known as ‘mortgagee in possession’) and sell it to regain the money they loaned you.

Sometimes, there is a shortfall between what the property sells for, and what you owe the bank.

In order to sell your property, your lender will have to pay a number of fees and expenses: real estate agent and legal fees, which the lender needs to cover.

In this situation (when the lender is out of pocket), the lender will claim on your Lenders Mortgage Insurance to protect them from losses.

There are 2 main providers of LMI in Australia, or alternatively, some lenders provide their own LMI as well.

Two main providers of LMI:

Genworth (sometimes referred to as GE): for example: The CBA, NAB, Bank of Queensland and Westpac use Genworth as their mortgage insurer;

QBE Insurance: (Used by ANZ, Suncorp and BankWest.)

Each of these providers can have different policies relating to how and who they provide mortgage insurance too and the rates that they charge.

The LMI premium you pay is worked out between the insurance providers and the lender you are borrowing with.

This is why LMI premiums can vary by up to thousands of dollars.

Or alternatively, some lenders provide their own insurance (they will call it a different name but it essentially serves the same purpose ) and again there are large variations in what premium they charge (up to several thousand dollars).

When we’re recommending suitable home loans for your situation we are also taking into account the cost of the LMI as well.

My name is Victor Kalinowski, and I’m a Brisbane Mortgage Broker at Blackk Mortgage Brokers. As an experienced refinance broker, I can help you navigate the complexities of lenders mortgage insurance to ensure the best financial outcome for you and your financial goals. Explore our services today and join us on the path to secure and profitable property investment.

The information contained within this page is general in nature. It serves as a guide only and does not take into account your personal financial needs. Before you act on this information you should seek independent legal and financial advice. Copyright Blackk Mortgage Brokers 2026.

Victor Kalinowski

Mortgage Broker and Founder of Blackk

I’m Victor Kalinowski and a Brisbane Mortgage Broker at Blackk Mortgage Brokers. I’ve helped thousands of people get loans for their homes and investment properties.

99.9% Approval Rate

Insider advice to negotiate making a successful offer on a home

Award Winning Mortgage Broker

If you are happy with the service from your current lender, but would like a better deal.

Work with Victor, not with random brokers

If you are happy with the service from your current lender, but would like a better deal.

with 99.6% first time success rate

No Obligations

Subscribe to get tips on home loans and property straight to your inbox

By downloading you agree to receiving occasional and only useful emails from us.